Disclaimer: I am not a financial advisor, the info on this site is for educational purposes. All investing decisions should be based on your own research. Opinions expressed here are my personal views and should not be taken as financial advice.

Living paycheck to paycheck is one of the most stressful financial positions to be in. You’re constantly waiting for your next direct deposit, scrambling to pay bills, and hoping nothing unexpected pops up before payday. But millions of Americans are in this exact position, and the good news is, there is a way out.

According to a 2024 report from LendingClub, 65% of U.S. adults reported living paycheck to paycheck. That includes many people earning over $100,000 per year. It’s not always about how much you make. It’s about how you manage what you have. These nine steps will help you take control, stabilize your situation, and finally move forward.

Article Highlights

- Identify and fix what’s draining your money the fastest

- Increase income while controlling spending habits

- Build savings and avoid falling back into old patterns

1. Assess the Problem Honestly

You can’t fix what you won’t face. If you’re living paycheck to paycheck, you have to start with brutal honesty. Where is your money going? What are the habits, bills, or decisions that keep draining your account every month?

Sit down with your bank and credit card statements from the last 60 days. Go line by line and categorize everything. You’re looking for patterns, recurring charges, and financial blind spots. Are you paying for five streaming services? Eating out four times a week? Is debt eating up half your income? This step isn’t about guilt. It’s about awareness.

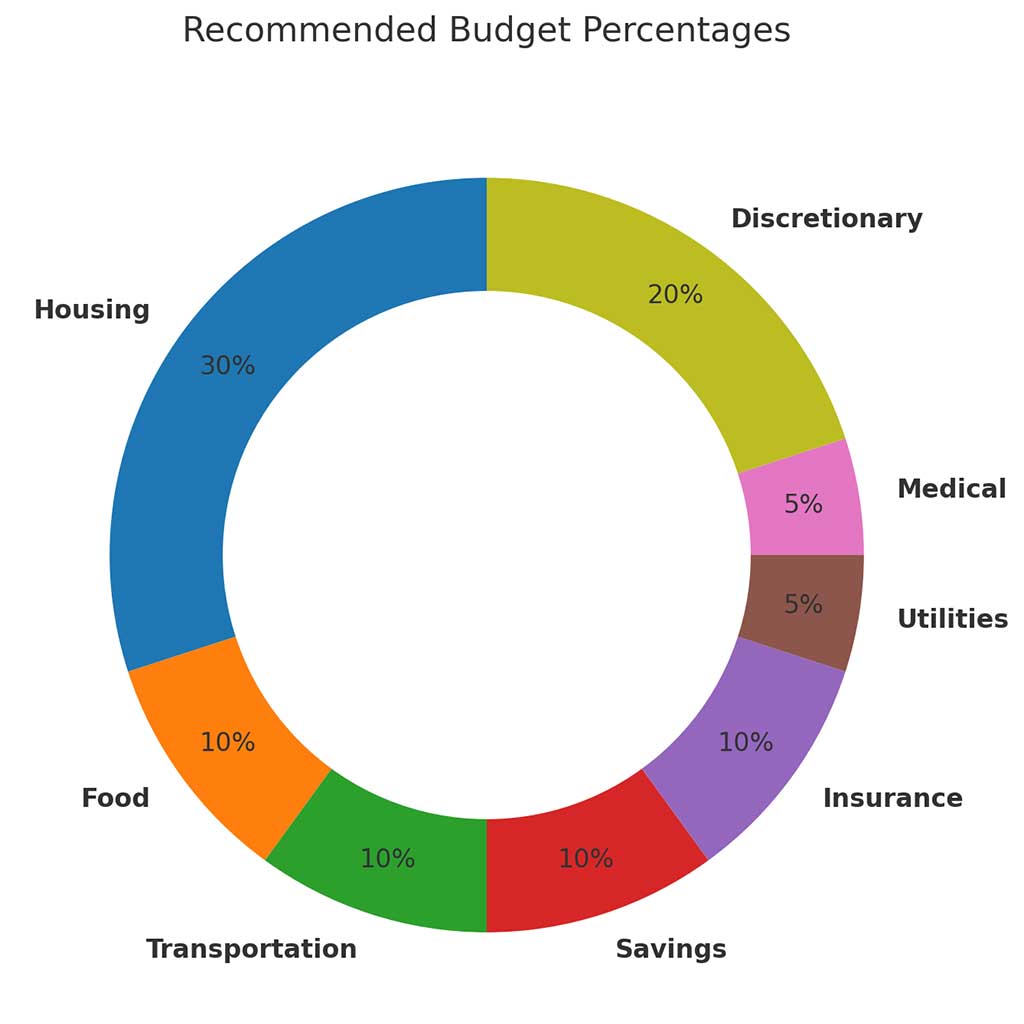

Below is a simple breakdown to help you spot where your money might be bleeding. These percentages may not be exactly where you end up and are more for example.

2. Fix the Root Cause (Or Cut It Out)

Now that you know what’s causing the cash flow issue, you have to act. It’s time to make hard decisions. If your housing is eating up half your income, it may be time to downsize or find roommates. If your partner spends more than you can afford, it’s time for an honest conversation and possibly shared financial tracking.

This is where most people stall because the fixes aren’t always comfortable. But the faster you deal with the root cause, the faster your situation improves.

Common financial leaks to consider cutting or adjusting:

- Rent or mortgage too high for your income

- Car loan or lease that’s killing your monthly budget

- Daily takeout or frequent dining out

- Subscriptions you barely use

- Uncontrolled impulse spending

Stopping the leak is the most powerful thing you can do. You can’t build savings if your income disappears the moment it lands.

3. Make More Money

Bringing in more income makes every other step easier. It’s not just about managing your budget. It’s about having more room to breathe.

If your current job doesn’t pay enough, start applying elsewhere. Even a $2 per hour raise adds up to over $3,000 per year before taxes. Consider side hustles, weekend gigs, or starting something small from home that fits your schedule.

You don’t need to build a six-figure business overnight. You just need to tip the balance in your favor. If you have a partner, they should also be contributing as part of the solution. Two steady incomes are better than one.

4. Build a Mini Emergency Fund

When you’re living check to check, any small emergency becomes a disaster. A flat tire or unexpected bill can wreck your entire month. That’s why you need a small buffer between you and crisis.

Start with a goal of $500 to $1,000. It’s not your full emergency fund yet, but it’s enough to prevent immediate panic when something goes wrong. Keep this money in a separate savings account, not your regular checking, so it’s harder to dip into casually.

Once you reach this goal, don’t stop. The more buffer you build, the more control you’ll gain.

5. Track Every Dollar

Tracking your money is about clarity, not control. You need to know where your cash is going before you can direct it better.

Apps like Mint, YNAB, or even a simple spreadsheet can help. Review your spending weekly. Categorize everything. This alone often changes behavior because once you see the waste, it’s harder to justify.

Aim for a system that takes 10 minutes or less to maintain. You don’t need perfection. You just need visibility.

6. Avoid New Debt

New debt keeps you stuck in the paycheck cycle. It adds future payments to an already strained budget and makes it harder to build any savings momentum.

Don’t open new credit cards. Don’t take out loans unless absolutely necessary. Don’t use buy-now-pay-later programs just to get by. If you already have debt, keep paying it down, but don’t add more to the pile.

The real win is staying steady and not digging the hole any deeper. Once you break the cycle, your money will go further.

7. Don’t Fall Back Into Old Habits

Getting ahead once is great. Staying ahead is the real goal. Many people escape the paycheck-to-paycheck cycle for a few months, only to fall back into the same trap. Usually, the reason is lifestyle creep.

When you earn more, don’t immediately upgrade your car, your wardrobe, or your apartment. Remember what it felt like when you were stressed about money. Use that as motivation to keep your budget tight and your goals in sight.

Write down a few financial habits that got you into trouble and post them somewhere visible. Remind yourself not to repeat them.

8. Save Aggressively and Catch Up

If you’ve been stuck in survival mode for a while, you’re likely behind on long-term savings. That’s okay. The best thing you can do now is focus on catching up, one month at a time.

Start by saving 10% of your take-home pay. Once that feels doable, try 15% or more. Increase your savings rate every time your income goes up. Automate your savings so it happens before you even see the money.

This is how you buy freedom. Freedom from stress. Freedom from emergencies. Freedom to quit a job or say no to something that doesn’t serve you.

9. Set a Short-Term Goal to Build Momentum

Pick something small and specific to work toward in the next 30 days. It could be:

- Save $100

- Pay off a single bill

- Sell something for extra cash

- Apply to five better-paying jobs

A win, no matter how small, builds confidence. It proves to you that change is possible. That feeling is fuel. Stack small wins and you’ll be shocked at how fast your situation turns around.

💡 Explore our free financial tools:

- Salary increase calculator – see how a raise will impact your paycheck or annual income.

- Compound interest calculator – see how small investments grow over time.

- Debt payoff calculator – find out how long it takes to pay off your debt and what it’ll cost you.

- Subscription savings calculator – uncover the true cost of forgotten subscriptions.

- Student loan payoff calculator – plan student debt payments that fit your budget.

- Retirement investment calculator – check if your savings plan supports your retirement goals.

- Emergency fund calculator – learn how much cash to keep aside for peace of mind.

- Impulse buy calculator – double-check if those purchases are really worth it.

- Mortgage refinance calculator – see how refinancing could lower payments or save interest.

- Mortgage affordability calculator – find out how much house you can afford with your budget.