Disclaimer: I am not a financial advisor, the info on this site is for educational purposes. All investing decisions should be based on your own research. Opinions expressed here are my personal views and should not be taken as financial advice.

If you’re wondering, “Can you use student loans for anything?” the short answer is yes, but that kind of freedom can lead to big mistakes. I’ve been there myself, using leftover loan money for things that felt necessary at the time but ended up costing me years of repayment. It’s easy to overspend when no one is checking, but it’s much harder to live with the consequences. In this article, we’ll break down what student loans are meant for, what you can legally use them for, and why being smart about it now can save you a lot of money later.

- Student loans can be used for almost anything once refunded to you

- That freedom is exactly what leads many people into deeper debt

- Every dollar borrowed has a long-term cost, and it adds up fast

What student loans are meant to cover

Student loans are designed to support your education, not your lifestyle. They exist to help you access and complete your degree, not to fund everyday spending with borrowed money.

The government defines eligible costs as “qualified educational expenses.” These are the essentials you need to enroll in school, stay in school, and graduate.

7 things that student loans are truly meant to cover

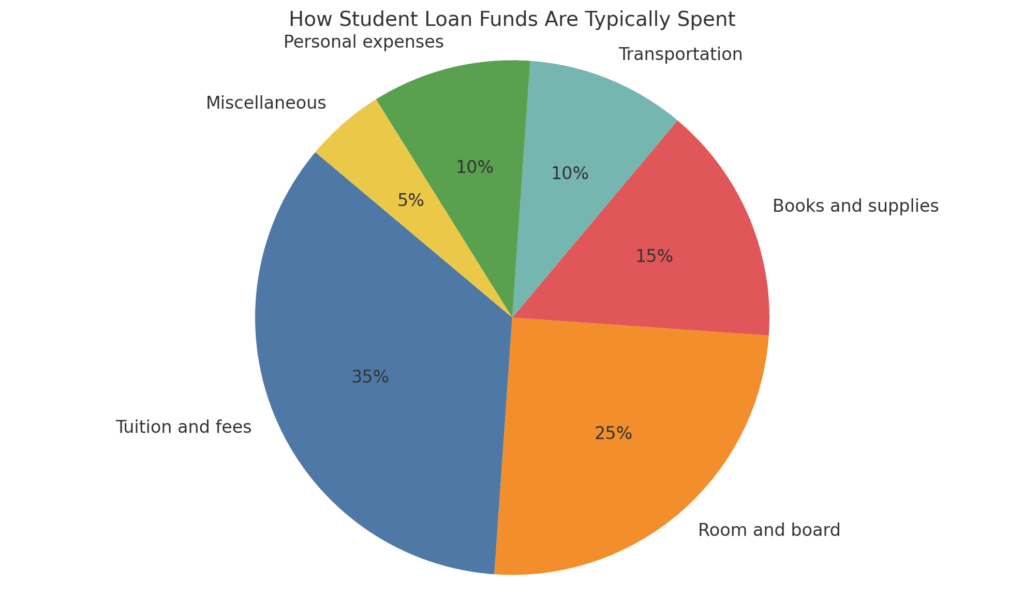

- Tuition and required fees

- On-campus or approved off-campus housing

- Meal plans or basic grocery costs

- Textbooks, lab supplies, and course materials

- A computer and reliable internet service

- Transportation to and from school (public transit or gas)

- Childcare expenses for dependent students

Each of these has a direct impact on your ability to attend and succeed in your program. Without housing, you may not be able to stay enrolled. Without textbooks or software, you can’t complete assignments. The point of student loans is to remove those barriers, not to pad your lifestyle.

The challenge is that once the money is disbursed, no one checks how you use it. That’s where many students get into trouble. It’s easy to blur the line between necessary and convenient. Is a new laptop required, or would a used one work just as well? Do you need your own apartment, or could you split rent with roommates and save a few hundred dollars a month?

Things like basic monthly living expenses can be covered by student loans, but they come with a major caveat. These everyday expenses can add up fast, especially if you start living like the loan money is free cash. That brings us to the next section: what you can use student loans for, but probably should avoid if at all possible.

Things you can loan money for (but maybe shouldn’t)

After your school deducts tuition and fees, any leftover loan money gets refunded to you. That refund is yours to manage, and technically, you can spend it however you want. No one is checking whether it goes toward books or a weekend getaway. It’s often thousands of dollars just dumped in the lap of a young college student. Things can be tempting.

This is also where things can get a bit blurry. Some non-tuition expenses are still connected to your ability to stay in school, and while they’re not officially tracked, they’re often treated as reasonable uses.

4 things student loans can be used for (if necessary)

- Rent or utilities

- A basic laptop for schoolwork

- Groceries or meal prep

- Gas or public transit for commuting

These are reasonable uses if you truly need help covering your living costs. If you can’t afford these things, you can’t continue school… so you have no choice but to pay for them by any (legal) means necessary.

The issue is when those needs blur into wants. It’s easy to justify ordering out, upgrading your tech, or spending casually because the money feels like it’s “already there.” I’ve done it. A few Amazon splurges, too many takeout nights, and the mindset of “I’ll figure it out later” turned into years of extra debt that could have been avoided.

Student loans aren’t free money. You’ll repay every dollar… with interest. These everyday costs seem harmless in the moment, but they add up fast. And once repayment kicks in, you’ll be paying for groceries and gas from years ago, long after the food is gone and the tank is empty.

That’s why student loans should be avoided if possible, but if you must, even the “allowable” expenses should be approached with caution. Just because you can use loan funds to cover them doesn’t always mean you should, get a part time job to help pay for your bills if you can.

Next we look at where that line of “what’s ok to spend my student loans on” gets crossed, and the kinds of spending that could cost you the most down the line.

Stuff you shouldn’t use student loan money for

Just because you can use student loans for anything doesn’t mean it’s a good idea. There’s a line where spending shifts from necessary to reckless, and once you cross it, you’re just borrowing money to make life more comfortable in the moment, at the expense of your future.

Student loans shouldn’t be used to fund your social life, upgrade your lifestyle, or pay for things that won’t move you closer to graduation. These are the kinds of purchases that bring short-term satisfaction and long-term regret.

Remember, you can’t wipe out student loans in bankruptcy unless you prove extreme financial hardship… and that’s very rare. Here are some of the main things to avoid spending on.

5 things you should never use student loans for

- Vacation or travel

- Electronics you don’t need for class

- Streaming services or shopping sprees

- Paying off unrelated credit card debt

- Giving money to friends or family

I know the temptation. It feels like extra money, especially when you’re stressed or strapped. But when that balance balloons with interest and you’re years into repayment, those spending choices feel a lot heavier.

The worst part is that none of those expenses help you graduate, get a job, or improve your financial future. You’re stuck paying them off without anything to show for it. That’s where over-borrowing becomes a real problem, and we’ll break that down next.

The real cost of overborrowing

It’s easy to shrug off student loan debt when the money feels like a lifeline. But every dollar you borrow today will come back with interest. That interest adds up fast, and most people don’t realize how much they’re actually signing up to repay.

Let’s say you borrow just a little extra each semester to cover things like groceries, gas, or rent. Over a four-year degree, that can quietly balloon into a major financial burden.

Here’s how student loan debt really adds up. The below loans are all at a pretty standard 6.5% interest rate, on a 10 year repayment term.

| Amount Borrowed | Total Repaid | Extra Paid in Interest |

|---|---|---|

| $10,000 | $13,854 | $3,854 |

| $20,000 | $27,708 | $7,708 |

| $35,000 | $48,489 | $13,489 |

| $50,000 | $69,271 | $19,271 |

| $75,000 | $103,906 | $28,906 |

And keep in mind, those numbers assume you make every payment on time, without delays. In reality, many borrowers go into forbearance, switch to interest-only plans, or simply fall behind. When that happens, interest keeps stacking up, and your loan balance may barely move even after years of steady payments. It’s not uncommon to pay thousands and still owe almost the same as when you started.

Smarter ways to handle living costs

When you’re juggling school, bills, and daily expenses, using student loan money to cover the gaps might feel like the easiest option. But the more you borrow, the longer and harder repayment becomes. If there’s any way to reduce how much you need to pull from loans, it’s worth exploring.

Start with realistic cuts

Take a hard look at your actual monthly expenses. Are you living in the most affordable housing option you reasonably can? If you’re living alone, sharing rent with roommates could instantly cut your monthly cost in half. If you’re commuting, look into public transportation passes or carpooling to save on gas and maintenance.

Food spending is another area with huge potential. Skip the meal delivery apps and start meal prepping. Even simple plans like cooking once and eating leftovers for a few days can make a big dent in your grocery bill. Many campuses also have food pantries or free meal programs for students—don’t be afraid to use them.

Technology is another trap. You don’t need the newest laptop or phone to succeed in school. Buy used or refurbished if possible, or look into whether your college has tech lending programs or student discounts through major retailers.

Bring in extra help

If you’re not already working, a part-time job—even 8 to 12 hours a week—can give you enough to cover basic costs without touching loan money. Campus jobs often come with flexible hours and low stress. If you’re more entrepreneurial, freelance gigs like tutoring, editing, or tech support can be done on your own schedule.

You might also qualify for additional non-loan aid. Many students overlook grants, emergency assistance funds, or scholarships that are available beyond freshman year. Talk to your financial aid office—there may be options you didn’t even know existed.

Practical ways to reduce borrowing

- Take on a part-time or work-study job with flexible hours

- Share housing and utilities with others to cut costs

- Stick to a weekly grocery budget and cook meals at home

- Apply for scholarships, grants, or emergency student aid

- Use used books, free PDFs, or library resources instead of new textbooks

- Look for free or discounted student software and tech options

- It’s not about making life harder—it’s about avoiding unnecessary debt that will weigh on you for years. Every dollar you don’t borrow now is one you don’t have to repay later with interest.

Being smart about spending doesn’t mean you have to live on ramen or miss out on everything. It just means thinking ahead and asking yourself, “Will this still be worth it when I’m paying for it ten years from now?” If the answer is no, find another way to cover it.

The bottom line

Yes, you can use student loans for almost anything. That’s exactly what makes them risky if you’re not careful.

Every dollar you borrow is a dollar you’ll repay later, with interest. Only take what you truly need. If there’s money left over, return it to reduce your balance.

Student loans are a tool, not a paycheck. Used wisely, they can help you get through school and build a better future. Used carelessly, they can follow you for years and drain your finances long after graduation. Make every dollar count now so you don’t have to pay for it twice later.

💡 Explore our free financial tools:

- Salary increase calculator – see how a raise will impact your paycheck or annual income.

- Compound interest calculator – see how small investments grow over time.

- Debt payoff calculator – find out how long it takes to pay off your debt and what it’ll cost you.

- Subscription savings calculator – uncover the true cost of forgotten subscriptions.

- Student loan payoff calculator – plan student debt payments that fit your budget.

- Retirement investment calculator – check if your savings plan supports your retirement goals.

- Emergency fund calculator – learn how much cash to keep aside for peace of mind.

- Impulse buy calculator – double-check if those purchases are really worth it.

- Mortgage refinance calculator – see how refinancing could lower payments or save interest.

- Mortgage affordability calculator – find out how much house you can afford with your budget.